Benefits of Owning a Home vs Renting: Investing in Yourself

The benefits of owning a home instead of renting offer buyers several tax advantages, the ability to grow equity, and of course a place to call your own. It’s also a feel-good milestone that offers a sense of pride and accomplishment. And, the current real estate and mortgage market conditions have created the perfect opportunity to transition from writing a monthly rent check to investing in your own home.

Check out these ten benefits of owning a home. See why it may be the best financial decision you can make, and learn some key tips on how you can get there affordably.

10 reasons to stop renting and buy a home

1. Rents continue to increase

The cost of rent has increased at a very fast rate throughout the country. This trend is only expected to continue. In fact, research from the Urban Institute shows rent in many markets has grown much faster than median incomes. The high cost of rent means that paying a monthly mortgage is often comparable to or even cheaper than renting a home. Don’t believe it? Find out for yourself. Zillow’s Rent vs. Buy Calculator can show you how many years it will take before the cost of buying equals the cost of renting – or, the break-even horizon.

2. Homeownership is a better long-term investment

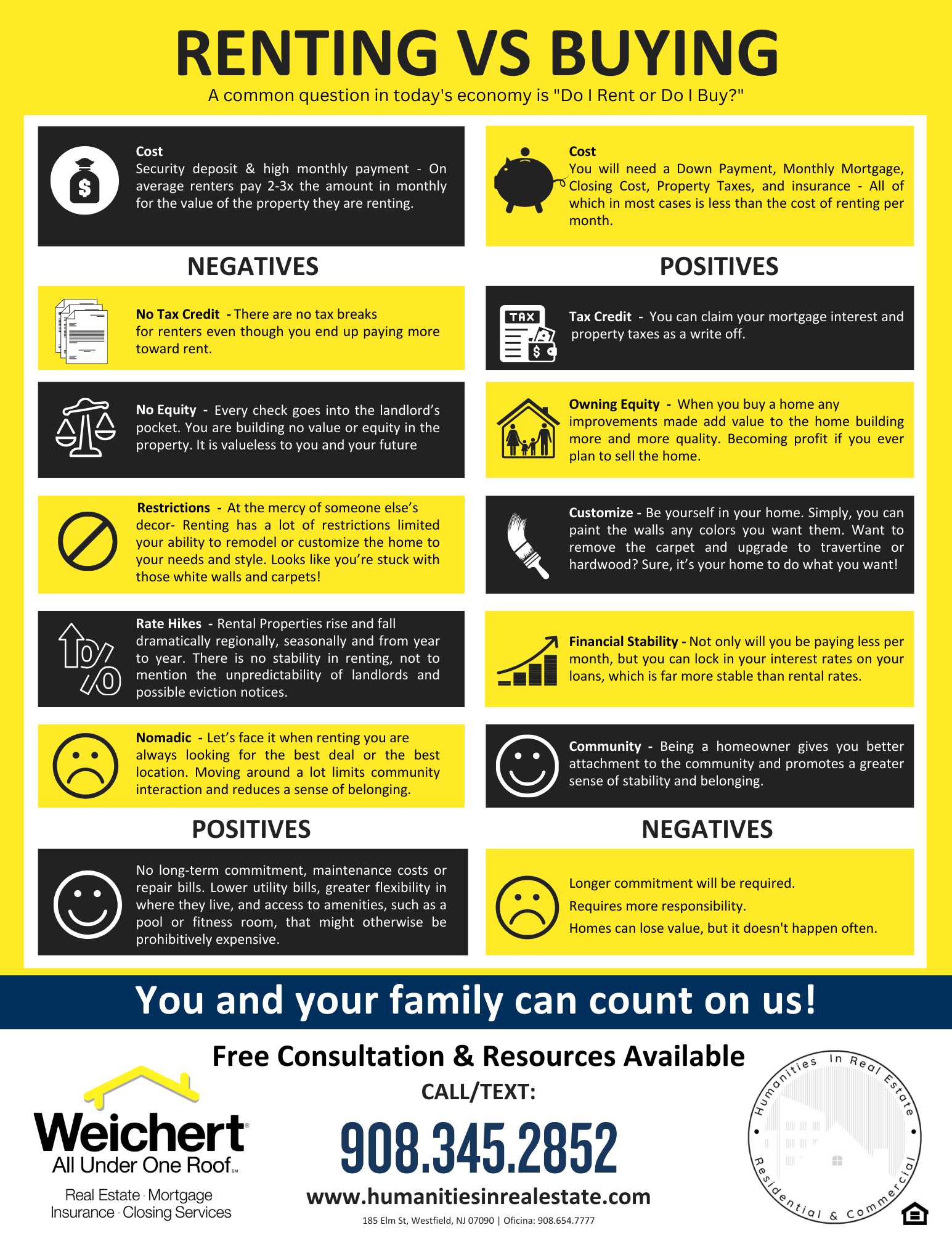

Renting your home means paying your landlord and having nothing to show for it the next month. Home ownership is a great investment because it’s a method of forced savings. When you buy a home with a 30-year mortgage and make monthly payments, you will own a home to sell at the end. If you rent a property for 30 years, however, you won’t ever get any of your monthly rent payments back.

3. Interest rates are historically low

The argument for buying instead of renting only gets stronger with the low-interest rates that are currently available. What may seem like a slight difference in your mortgage rate can make a huge difference in your monthly payment. Interest rates are still competitively low. So, now is a great time to purchase a home and take advantage of low rates. Locking into a low 30-year mortgage rate today could save you hundreds of dollars each month for decades to come. When comparing the benefits of owning vs. renting, you will find that many of the current rental rates are higher than a mortgage payment, and you do not get the advantage of a yearly tax deduction.

4. Down payments can be as little as zero dollars

Sound too good to be true? It's not. There are loan programs and government assistance programs that can get qualified home buyers into a home with a zero dollar down payment. Now, that does not necessarily include closing costs, so keep that in mind. Programs vary by lender and borrowers must meet certain requirements. Yet, if you're looking to buy a home with no down payment, look at a VA loan (for veterans, active duty military, military spouses), a USDA loan, or the Chenoa Fund.

5. Gift money can be used as a down payment

That $25 check from Grandma is always a nice little birthday gift. Now what if Grandma, or any family member, could gift you just a bit more. Something that can add up and be used toward down payment on your own home. Is that even a thing? Believe it or not -- using gift money for down payment is allowed. The amount you’re eligible to receive depends on your loan program. There’s a good chance you may have to come up with your own money to help cover the cost of down payment, but it's a heck of a lot less than you'd need to come up with on your own.

6. Gain equity as property values continue to rise

Home values have risen and are expected to continue rising in the future, making homeownership a profitable long-term investment. In the past year alone, home prices have risen 13.2%. Why does this matter? Because increasing property values mean that the money you spend on your home will provide significant returns in the long run. And, every time you make a mortgage payment, a portion of that payment pays your loan down each month, giving you more equity in the home.

7. Higher loan amounts

Housing inventory recently fell to a two-year low. Even with favorable mortgage rates, a first-time home buyer will likely struggle to find a residence they can afford. However, thanks to higher loan amounts on conforming loan programs, you're able to finance more home.

8. Predictable monthly payments

Tired of your rent rising? Sick of it causing your budget to change? When owning a home, and using a fixed-rate mortgage, that can never happen. You’ll always pay the same amount each month, each year. Plus, there's no risk of a landlord trying to kick you out because he wants to sell the home. Want a better idea of what to expect? Use our simple mortgage monthly payment calculator to estimate your monthly mortgage payment for a new home loan. Enter a home price, your expected down payment, and desired loan term to get an estimated monthly breakdown of payments.

9. Bring in extra income by renting a room

Being a homeowner means you have an opportunity to earn extra income by renting out a room. Maybe you bring in a long-term tenant to rent out your basement, or you look at short-term tenants via renting a room on Airbnb. As a homeowner, everything is completely up to you -- how much you charge, how often you have someone renting from you, etc. There's no landlord to ask permission from or roommate that needs convincing.

10. Tax deductions

Being a homeowner does not have to be just a long-term aspiration. Enjoy short-term savings via annual tax write-offs and mortgage interest payment deductions, along with other deductions depending on each individual’s situation. These deductions often amount to significant savings, and they are of course not available to renters.

With all of the benefits of owning a home, you owe it to yourself to find out whether owning vs. renting is best for you. Taking the simple step of speaking to a qualified mortgage lender may be the smartest financial situation you make, as it can allow your family to make monthly home payments toward your own asset instead of increasing your landlord’s wealth.